4 3: Record and Post the Common Types of Adjusting Entries Business LibreTexts Leave a comment

No, your accountant is making up for a mistake they made last financial period. We can break down steps five and six of the accounting cycle into a bit more detail. 11 Financial is a registered investment adviser located in Lufkin, Texas.

Why Adjustments Are Needed?

Deprecation is the practice of expensing the value of a capital asset over the period of its useful life to align with the matching principle. Accruals are used for transactions that have occurred but where cash hasn’t yet changed hands. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career. — Paul’s employee works half a pay period, so Paul accrues $500 of wages. Recall the transactions for Printing Plus discussed inAnalyzing and Recording Transactions.

- They are used to reflect cash transactions that have already taken place but which need to be recognized in future accounting periods.

- For example, if a company has recognized revenue that has not yet been earned, an adjustment entry is made to remove this revenue from the income statement.

- You can always increase the frequency based on your company’s specific needs.

- Adjustment entries can also impact a business’s stock-based compensation expenses.

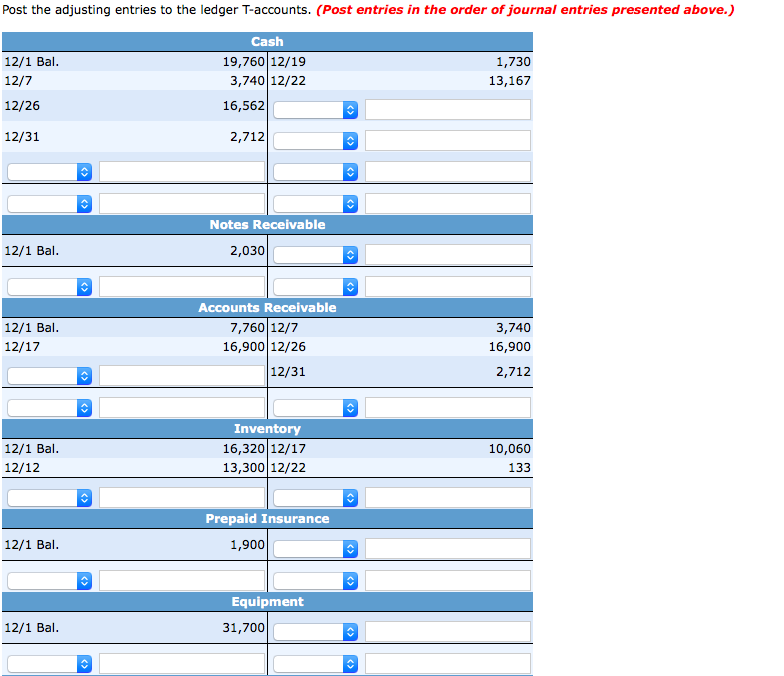

- Following is a summary showing the T-accounts forPrinting Plus including adjusting entries.

Communicate Effectively with Employees

Accruals are revenues and expenses that have not been received or paid, respectively, and have not yet been recorded through a standard accounting transaction. For instance, an accrued expense may be rent that is paid at the end of the month, even though a firm is able to occupy the space at the beginning of the month that has not yet been paid. The four types of adjustments in accounting include accruals, deferrals, reclassifications, and estimates. Accruals and deferrals involve adjusting entries to record transactions that have occurred but have not yet been recorded.

Your Revenue Reporting May Be Inaccurate

Thus, every adjusting entry affects at least one income statement account and one balance sheet account. Adjusting entries are made at the end of an accounting period after a trial balance is prepared to adjust the revenues and expenses for the period in which they occurred. In this chapter, you will learn the different types of adjusting entries and how to prepare them. You will also learn the second trial balance prepared in the accounting cycle – the adjusted trial balance. Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. If you use accounting software, you’ll also need to make your own adjusting entries.

What is the approximate value of your cash savings and other investments?

It represents the amount that has been paid but has not yet expired as of the balance sheet date. The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31. The balance sheet is also referred to as the Statement of Financial Position. Therefore, the entries made that at the end backward inhibitory learning in honeybees of the accounting year to update and correct the accounting records are called adjusting entries. The process of recording such transactions in the books is known as making adjustments. An adjustment can also be defined as making a correct record of a transaction that has not been entered, or which has been recorded in an incomplete or incorrect way.

These entries can impact a business’s cash flow, profitability, stock-based compensation, accounting periods, and fiscal year. Adjustment entries can also impact a business’s profitability by affecting the amount of revenue and expenses that are recorded in a particular accounting period. For example, if an adjustment entry is made to increase revenue, this will increase the business’s profitability for that period. Conversely, if an adjustment entry is made to increase expenses, this will decrease the business’s profitability for that period. Prepaid insurance is insurance that has been paid for but not yet used.

You can always increase the frequency based on your company’s specific needs. Adjustment entries are crucial in ensuring that financial statements accurately reflect the financial position of a company. Adjustment entries are an essential part of financial statements, particularly in the balance sheet and income statement. These entries are made at the end of an accounting period to ensure that the financial statements accurately reflect the company’s financial position and performance.

The adjusting entry will debit Interest Expense and credit Interest Payable for the amount of interest from December 1 to December 31. In such a case, the adjusting journal entries are used to reconcile these differences in the timing of payments as well as expenses. Inaccurate financial statements can misrepresent your company’s financial health, potentially impacting investor confidence and access to funding. Miscalculations can also lead to disputes with employees regarding their earned time off, affecting morale and potentially leading to legal issues. Non-compliance with accounting standards and labor laws can result in penalties and legal action.

Adjusting entries will play different roles in your life depending on which type of bookkeeping system you have in place. Get free guides, articles, tools and calculators to help you navigate the financial side of your business with ease. The magic happens when our intuitive software and real, human support come together.